"We Should Sell To Self-Insured Employers"

Get Out-Of-Pocket in your email

Looking to hire the best talent in healthcare? Check out the OOP Talent Collective - where vetted candidates are looking for their next gig. Learn more here or check it out yourself.

Hire from the Out-Of-Pocket talent collective

Hire from the Out-Of-Pocket talent collectiveHealthcare 101 Crash Course

%2520(1).gif)

Featured Jobs

Finance Associate - Spark Advisors

- Spark Advisors helps seniors enroll in Medicare and understand their benefits by monitoring coverage, figuring out the right benefits, and deal with insurance issues. They're hiring a finance associate.

- firsthand is building technology and services to dramatically change the lives of those with serious mental illness who have fallen through the gaps in the safety net. They are hiring a data engineer to build first of its kind infrastructure to empower their peer-led care team.

- J2 Health brings together best in class data and purpose built software to enable healthcare organizations to optimize provider network performance. They're hiring a data scientist.

Looking for a job in health tech? Check out the other awesome healthcare jobs on the job board + give your preferences to get alerted to new postings.

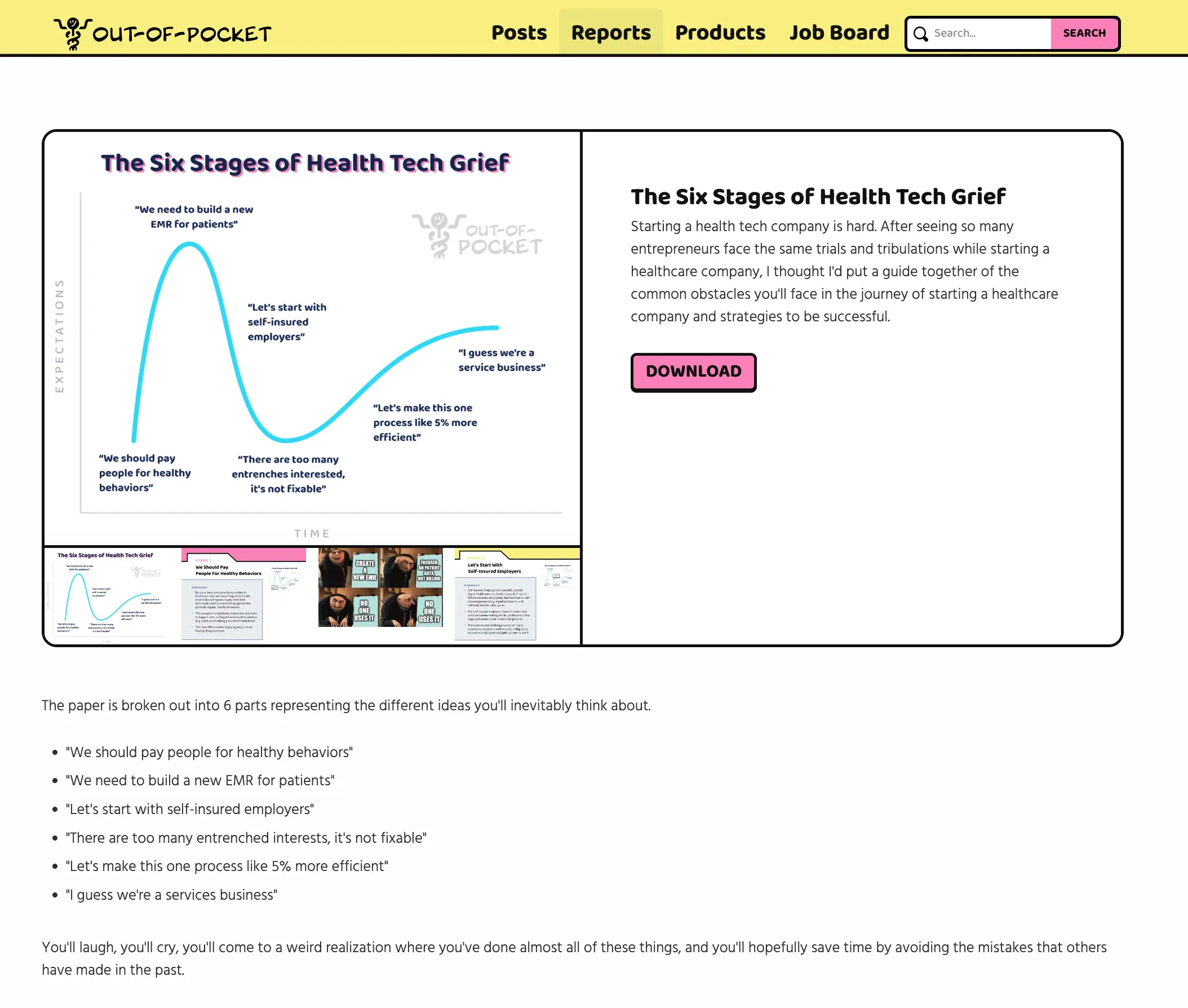

The full white paper with all six parts of this series (nice, cleaned up, and formatted) can be found here.

---

Last week, I went through the first two parts of this graphic. Today I want to focus on the third step: selling into self-insured employers.

“Let’s Start With Self-Insured Employers”

Usually what happens is people new to healthcare will discover (generally) that

- There’s a low willingness to pay from consumers.

- Hospitals also have a low willingness to pay unless it’s related to getting them more money (aka. patient referrals or increasing billing/reimbursement).

- Insurers want proof that your solution works and have a super long sales cycle.

This creates a Catch-22. How can you find customers to demonstrate your solution works when no one that will try the solution? Some people might enter pilots with hospitals or insurers, but in many cases those are destined to fail without real internal buy-in (and therefore internal resources) and/or are given small test populations that may not work for some reason intrinsic to that population.

Plus, just because you run a pilot with somebody doesn’t mean they necessarily have to become a customer. There’s a graveyard full of “death by pilot” startups, where the company is used as a case study but not as a long-term partner.

Enter the self-insured employer (primer here). You probably looked at some of these cute surveys about employers wanting to adopt new health solutions and employees wanting to use more healthcare services and thought to yourself “holy shit I’m the first person to notice this, I’ve cracked the code”.

On the surface, going the self-insured employer route has a lot of benefits (nice). There’s a more straightforward/shorter sales cycle vs. selling to health insurance carriers, including a built-in distribution channel via benefit brokers if you go that route. Plus, there’s a generally higher willingness to test out low-risk products that will reduce spend or increase employee satisfaction.

So the obvious plan is to go to some self-insured employers, prove the value and get some data, then go to larger self-insured employers or the insurance companies with data in hand. Healthcare is easy.

Some things companies will discover when going down this route.

The sales and distribution problem

Customers are very concentrated in the employer segment. About 4% of plans cover 65% of total lives. The big companies are mad big.

Even amongst them, not a ton of those employers are super willing to try new solutions. You know it’s bad when Comcast is considered one of the more innovative companies in plan design and trying solutions…

The innovative employers see a million identical pitches for the same solution every quarter. This channel is way more saturated than companies think - no employer wants to hear another pitch where the entire value proposition is “give your employees telemedicine so they avoid ER visits”. There’s A LOT of those companies already.

The sales cycles into self-insured employers is extremely varied as well. It can be super short, or extremely long, and the process for each company is going to be really different. As an example, diabetes management company Livongo Health, has an average sales cycles of less than 6 months with some deals taking less than a month and some taking more than 12.

And you have to make sure you catch these employers when they’re setting up the following year’s budgets, otherwise you’re going to have to wait till the next cycle. If you’re trying to DISPLACE an existing solution that’s already in place, the burden of proof is even higher because most employers would rather just press the “auto-renew” button.

Part of this sales process includes figuring out who is actually doing the diligence for your solution. In smaller companies it might just be the head of benefits doing everything, and many times they aren’t healthcare experts but are thinking about compensation more holistically.

In most cases, self-insured employers will rely on benefits consultancies like Mercer, Aon, Willis-Towers Watson, etc. to help them come up with overall employee compensation plans that make the most sense, which will include health benefits along with life insurance, 401ks, etc. Some digital health startups will choose to partner with these benefits companies, but these channels are more saturated than most companies realize and some brokers have…interesting commission structures that need to be navigated.

There haven’t been too many big successes that have scaled solely via the self-insured employer route, and almost all of them have used a benefits partner to get there (Livongo-Mercer, Castlight-Willis, Hinge Health-Meritain, Grand Rounds-Mercer, etc.).

You could instead partner with one of the health insurance companies that sell non-health insurance products to employers (e.g. the plans that act as an administrator for the employer), but then you’ll hit the same exact problems around selling into health insurers.

{{interlude 3}}

Contract in hand ≠ Success

Even once you get the contract in hand with an employer, you actually have to get their employees to use the product. Livongo says in their investor documents that these implementations take about 3 months, and takes 12 months to get to 34% of total recruitable individuals. Exits & Outcomes excellent enrollment report talks about several issues that companies selling into employers have to deal with when reaching out to employees, including not having company emails.

“During a recent deployment with an innovative aeronautics company, we brainstormed ways to connect with every employee. The challenge? Get a compelling message to a team without company email addresses. The solution? Identify the locations everyone visited each day. That left us two good options: the cafeteria and the bathroom. We chose the former. We co-opted the napkin dispensers for one week to share bold, inspiring messages about the new benefit, all in the voice of the company’s leader.” - Omada Health

If you don’t get employees to engage, guess who’s not getting a contract renewal? Getting the employer on board to try a solution is only half the battle - each employer is going to have their own unique issues when you want to roll out your service. Getting the second or third year contract is harder than a lot of companies realize since you actually have to prove that you managed to enroll their employees into your solution, have them use it when they need to, and then figure out some metric of success that was achieved with a $ value like avoided surgeries, or amount saved by routing an employee to certain pharmacy/hospital.

It’s not just about getting any people into your programs, but the people that will ACTUALLY save the company money. In a study of a 12,000 employee company in Illinois, they found that most of the people that opted into their workplace wellness programs were the people that already had low health spend. That makes this program a nice perk for the company, which can still be valuable, but it’s not actually a health solution and should be evaluated on different metrics (e.g. employee satisfaction).

So while employer channels may seem like they solve all your problems - they actually just present a host of their own and are harder to crack into than you think.

Good parts of the employer channel

Selling into the employer channel does offer some interesting benefits though:

- There’s an inherent office virality that happen when coworkers start talking about a benefit (e.g. many coworkers would recommend One Medical to each other when a new employee asked about an in-network PCP)

- Bringing services to offices not only reduces friction by bringing healthcare to where people already are, but there’s added social pressure to partake (e.g. when flu shots come to the office).

- Having an employer pay for a service that a consumer may not have paid for themselves helps alleviate the “Market For Lemons” problem. Many consumers aren’t sure if paying for some service is worth it until they try it, after which they become regular consumers. Then employees start suggesting it as a perk to future employers, which gives bottoms-up adoption and can help bypass brokers (or at least give your company more leverage when you talk to them).

The above is also only true for areas of health that people actually talk openly about, which tend to be preventive and screening instead of actual health issues that drive real healthcare spend.

Conclusion

In summary - employers can be a useful channel but it’s pretty saturated and won’t solve the underlying problems of your business if consumers weren’t finding you that useful to begin with. Plus, if you believe in a world where healthcare in the US isn’t reliant on the employer, then you’re playing a dangerous game building out all of your processes to center around the employer channel.

Thinkboi out,

Nikhil aka. Self-Insured Unemployer

Twitter: @nikillinit

P.S. If anyone is wondering how I’m handling COVID, I shaved my hair into a mohawk and I’m not totally sure when this joke is supposed to end. I miss barbers. And trying to look presentable.

{{sub-form}}

---

If you’re enjoying the newsletter, do me a solid and shoot this over to a friend or healthcare slack channel and tell them to sign up. The line between unemployment and founder of a startup is traction and whether your parents believe you have a job.

Interlude - Apply to Knowledgefest! And healthcare 101 starts next week!

See All Courses →Don’t forget the application for our Knowledgefest, our healthcare software engineering conference IS LIVE.

If you work in healthcare ops, you want to be here. This is where you learn playbooks, see what other ops people are doing, and build your network. It’s year 5 and we sell out every year - applications are due end of month.

And if you feel like you really need to get up to speed on how healthcare works, then you should let me teach you at Healthcare 101starting next week!This is for anyone hiring teams of non-healthcare people that need to get up to speed quickly (in 2 weeks) - we do group discounts too hit up ya boy. You’ll even learn how to make memes.

.png)

Get Out-Of-Pocket in your email